How Mortgage Rates Affect Your Monthly Payment in Bloomington MN: 3 Things Most Buyers Miss…

Mortgage Pre-Approval Bloomington MN: How It Works + What to Expect (2026 Guide)

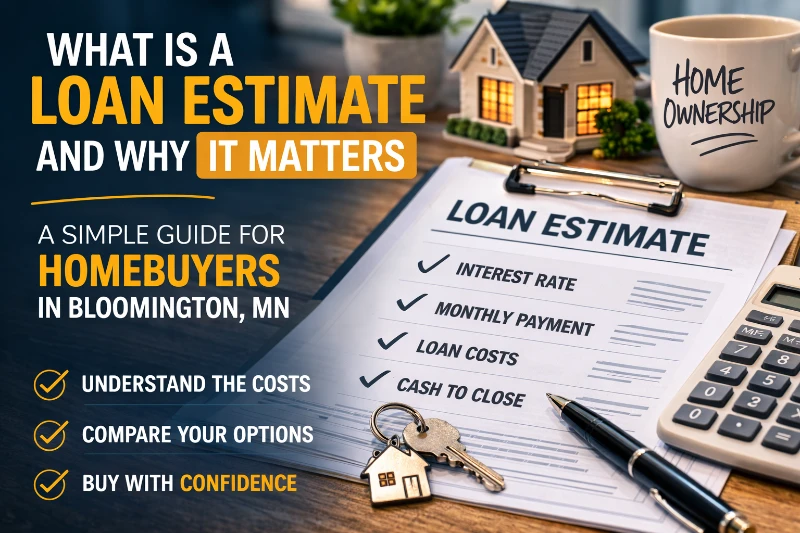

Mortgage pre-approval Bloomington MN is one of the smartest first steps you can take when buying a home.

Most buyers start by looking at homes first. That makes sense. It’s exciting.

A lot of buyers start by looking at homes first. That makes sense. It’s exciting.

But without knowing your numbers, it’s easy to either look too high… or hold back when you don’t need to.

Pre-approval brings clarity.

No guessing. No surprises. Just a clear picture of where you stand.

What Is Mortgage Pre-Approval?

Mortgage pre-approval is when a lender reviews your full financial picture and tells you what you can qualify for.

We’re looking at four main areas:

- Credit

- Income

- Assets

- Monthly debts

This is what we call the foundation of underwriting.

Once that’s reviewed, you get a pre-approval letter that shows:

- your estimated price range

- loan program options

- expected monthly payment

That’s what sellers and agents want to see when you submit an offer.

When you go through mortgage pre-approval Bloomington MN, the goal is not just getting approved. It’s making sure the loan actually fits your situation.

Why Mortgage Pre-Approval Matters in Bloomington MN

In a competitive market like Bloomington MN and the Twin Cities, pre-approval is not optional. It’s expected.

Here’s why it matters:

1. You know your real numbers

Not a guess. Not a calculator online. Real numbers based on your situation.

2. You move faster when the right home shows up

Homes don’t wait. Being prepared gives you an edge.

3. Your offer is stronger

Listing agents want confidence that your financing is solid.

4. You avoid surprises later

The goal is simple. No issues once you’re under contract.

How Mortgage Pre-Approval Works (Step by Step)

Here’s what the process looks like:

Step 1: Initial conversation

We talk through your goals, timeline, and what you’re trying to accomplish.

Step 2: Application

You fill out a secure application so we can review your full profile.

Step 3: Document review

This usually includes:

- pay stubs

- W-2s or tax returns

- bank statements

Step 4: Credit and numbers analysis

We review your credit and calculate your debt-to-income ratio.

Step 5: Pre-approval issued

You receive a pre-approval letter that you can use when making offers.

What Credit Score Do You Need?

This is one of the most common questions I get.

Here’s a simple breakdown:

- Conventional loans typically prefer 620+

- FHA loans can go lower depending on the situation

- VA loans are more flexible but still need strong overall approval

The bigger picture is this:

It’s not just your score. It’s how everything fits together.

How Much Can You Get Pre-Approved For?

This comes down to income, debts, and the structure of your loan.

As a general rule, lenders look at your debt-to-income ratio (DTI).

Most buyers fall somewhere under 45%, but every situation is different.

That’s why a real review matters more than an online estimate.

Common Mistakes to Avoid

A few things I see all the time:

- Starting home shopping before getting pre-approved

- Making big purchases before closing

- Changing jobs during the process

- Only talking to one lender without comparing options

A simple second opinion can make a big difference here.

Mortgage Pre-Approval vs Pre-Qualification

These get confused a lot.

Pre-qualification is a quick estimate based on what you tell the lender.

Pre-approval is verified.

That’s why sellers take pre-approval seriously.

Local Insight: Bloomington MN Buyers

In Bloomington MN, I see a lot of buyers who are closer than they think.

Some just need structure.

Some need the right loan program.

Some need a second look.

That’s where working with an experienced mortgage broker can open up more options.

If you’re curious where rates are sitting right now, I update mortgage rates in Bloomington MN weekly here:

https://kengraczak.com/mortgage-rates-bloomington-mn/

Final Thoughts

Mortgage pre-approval is not about pressure.

It’s about clarity.

When you understand your numbers, everything else becomes easier.

If you’re even thinking about buying, this is the place to start.

If you want a clear picture of where you stand, we can walk through it together.

Mortgage pre-approval Bloomington MN is not about pressure. It’s about clarity.

Mortgage Pre-Approval Bloomington MN: Common Questions

How long does mortgage pre-approval take?

Most pre-approvals can be completed within 24 to 48 hours once documents are submitted.

Does pre-approval affect your credit score?

Yes, it requires a credit pull, but the impact is usually small and temporary.

How long does a pre-approval last?

Most pre-approvals are valid for 60 to 90 days.

Can I get pre-approved without choosing a home?

Yes. Pre-approval is based on your finances, not a specific property.

Do I need pre-approval to make an offer in Bloomington MN?

In most cases, yes. Sellers expect it.

If you want to see how this works in real life, I break it down in a few short videos here:

https://www.youtube.com/@KenGraczak/shorts

For a simple breakdown of the homebuying and loan process, Freddie Mac has a helpful guide here:

https://myhome.freddiemac.com/

Related Posts