Mortgage Rates Bloomington MN: Why Rates Went Up and What It Means for Pre-Approvals (2026)…

All-In-One Mortgage Loan Bloomington MN: 2026 Guide (Is It a Smarter Way?)

All-In-One Mortgage Loan Bloomington MN: 2026 Guide to How It Works

If you’re looking into an all-in-one mortgage loan in Bloomington MN, you’re probably wondering if it’s a smarter way to pay off your mortgage faster.

The all-in-one mortgage loan Bloomington MN buyers ask about is becoming more common as people look for flexible ways to manage their mortgage.

That’s usually the question.

And it’s a good one.

Because on the surface, this sounds like a better way to manage your money.

But once you understand how it actually works, the answer becomes a lot clearer.

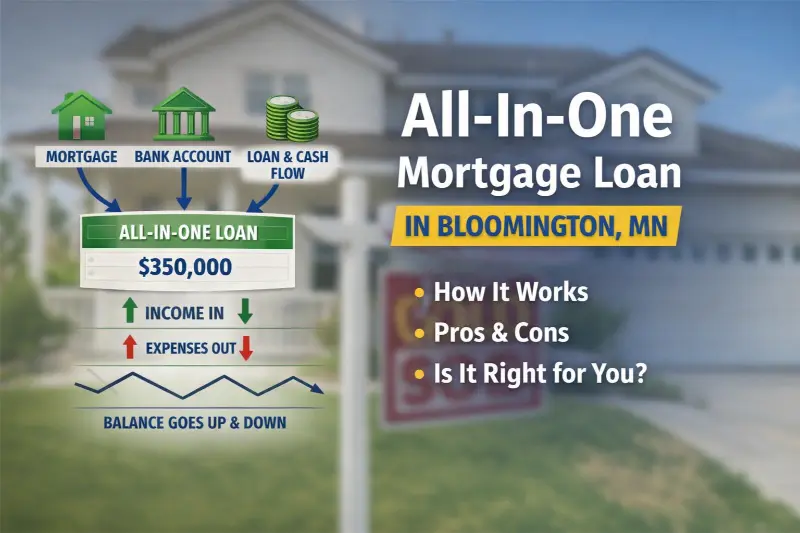

What Is an All-In-One Mortgage Loan?

The all-in-one mortgage loan Bloomington MN buyers ask about is really a HELOC used as your primary mortgage.

Now, instead of having:

- a mortgage payment

- a checking account

- a savings account

Everything runs through one place.

Your income goes into the loan.

Your expenses come out of the loan.

And your balance moves up and down as you use it.

How an All-In-One Mortgage Loan in Bloomington MN Works

Let me simplify this.

Interest is calculated daily based on your balance.

So when your paycheck hits:

- your balance drops

- you pay less interest

Then when you spend money:

- your balance goes back up

- interest adjusts again

So instead of a steady decline like a traditional mortgage…

your balance moves throughout the month.

For most people, the answer comes down to how they manage money day to day.

A Simple Way to Think About It

Let’s say you have a $400,000 loan and bring in $8,000 a month.

Normally, that $8,000 sits in your checking account.

It doesn’t do much.

With this setup, that same $8,000 sits against your loan balance.

So for part of the month, you’re paying interest on less.

That’s where the benefit comes from.

Why Do Some People Like This?

The idea is simple.

The more money sitting in the loan, the less interest you pay.

So if someone:

- keeps extra money in their account

- has steady income

- is intentional with spending

this can work in their favor.

But here’s the part most people don’t think through…

What Are the Downsides?

It’s an adjustable rate

This is not fixed.

So if rates go up, your cost goes up.

That matters.

There’s no built-in structure

With a traditional mortgage, the payment forces progress.

With this, nothing is forcing the balance down.

So let me ask you this:

If you have access to the money… will you leave it there?

That’s really what determines if this works.

It requires discipline

This works best for someone who:

- tracks their money

- avoids carrying debt

- keeps a cushion

If not, it can actually slow things down instead of speeding them up.

How Is This Different From a Regular Mortgage?

A traditional mortgage gives you structure.

- fixed payment

- predictable

- steady payoff

This gives you flexibility.

- balance moves daily

- interest adjusts daily

- payoff depends on behavior

Neither one is better.

It just depends on the person.

Does This Work for Buyers in Bloomington MN?

For most buyers I work with in Bloomington MN and across the Twin Cities, a traditional mortgage is still the better fit.

It’s simple. It’s predictable. It removes guesswork.

Where I do see this work well is for someone who:

- has strong, consistent income

- keeps cash on hand

- wants more control

For buyers here in Bloomington MN, the all-in-one mortgage loan can feel very different from what they’re used to.

That’s not a bad thing.

It just means it needs to fit the person.

Will This Help You Pay Off Your Mortgage Faster?

It can.

But only if you use it the right way.

If money stays in the account, interest goes down and the loan shrinks faster.

If money keeps coming back out, it may not make much difference.

That’s the part that usually gets missed.

Where Do the Rates Come From?

These loans are tied to variable rates and tend to follow broader market trends you’ll see from sources like

https://www.mortgagenewsdaily.com/mortgage-rates

and

https://www2.optimalblue.com/obmmi

The Better Question to Ask

Instead of asking:

“Is this better?”

A better question is:

“Would I actually use this the right way?”

Because the loan itself isn’t the advantage.

Your habits are.

If you’re comparing options, the all-in-one mortgage loan Bloomington MN strategy should always be looked at next to a traditional fixed mortgage.

Final Thoughts

This is one of those ideas that sounds really good at first.

And in the right situation, it is.

But it’s not a shortcut.

It’s just a different way to manage your mortgage and your cash flow.

If it fits how you already handle money, it can work well.

If it doesn’t, a traditional loan is usually the safer path.

If you’re considering an all-in-one mortgage loan in Bloomington MN, it’s worth taking a closer look at how you manage your money today.

Want to See If This Fits Your Situation?

If you’re in Bloomington MN or the Twin Cities and want to compare this to a traditional mortgage, I can walk you through both side by side.

No pressure. Just clarity.

FAQ

Is an all-in-one mortgage loan the same as a HELOC?

Yes. It is a HELOC structured to replace your mortgage and your bank account.

Are all-in-one loans fixed or adjustable?

They are adjustable. The rate can change over time.

Can this help me pay off my mortgage faster?

It can, but only if you consistently keep extra money in the account.

Is an all-in-one mortgage loan in Bloomington MN common?

Not yet. Most buyers still use traditional mortgages, but interest is growing.

What is the biggest risk with this type of loan?

The biggest risks are rising rates and lack of structure. If you are not disciplined, the balance may not go down as expected.

Related Posts